Dividend Aristocrats are S&P 500 ($SPX) listed companies that have increased their dividends for at least 25 consecutive years. These are often companies that have held up well over time, supported by steady cash generation, careful spending decisions, and leadership teams that have kept returning more cash to shareholders through all kinds of market and economic conditions. Out of roughly 70 companies that meet this standard, only a handful really separate themselves from the pack when looking at Wall Street analyst ratings. Walmart (WMT), The Coca-Cola Company (KO), and Nucor (NUE) consistently show up as three of the most highly rated dividend growers heading into 2026.

These stocks already come with the comfort of long dividend growth streaks, and their strong analyst ratings also point to potential upside, not just steady income. With stock valuations still elevated in many areas of the market and the economic picture still unclear, a mix of reliable dividend growth and positive analyst sentiment can offer a balanced setup for investors who prioritize income.

But what exactly sets these three companies apart from the other Dividend Aristocrats, and can their analyst ratings translate into real shareholder value in 2026? Let’s find out.

Walmart (WMT)

Walmart is the world’s largest retailer, built around massive scale across big-box stores, membership through Sam’s Club, and a fast-growing e-commerce business. More of its online growth is being supported by store-based pickup and delivery, which helps the company keep prices low while making shopping more convenient.

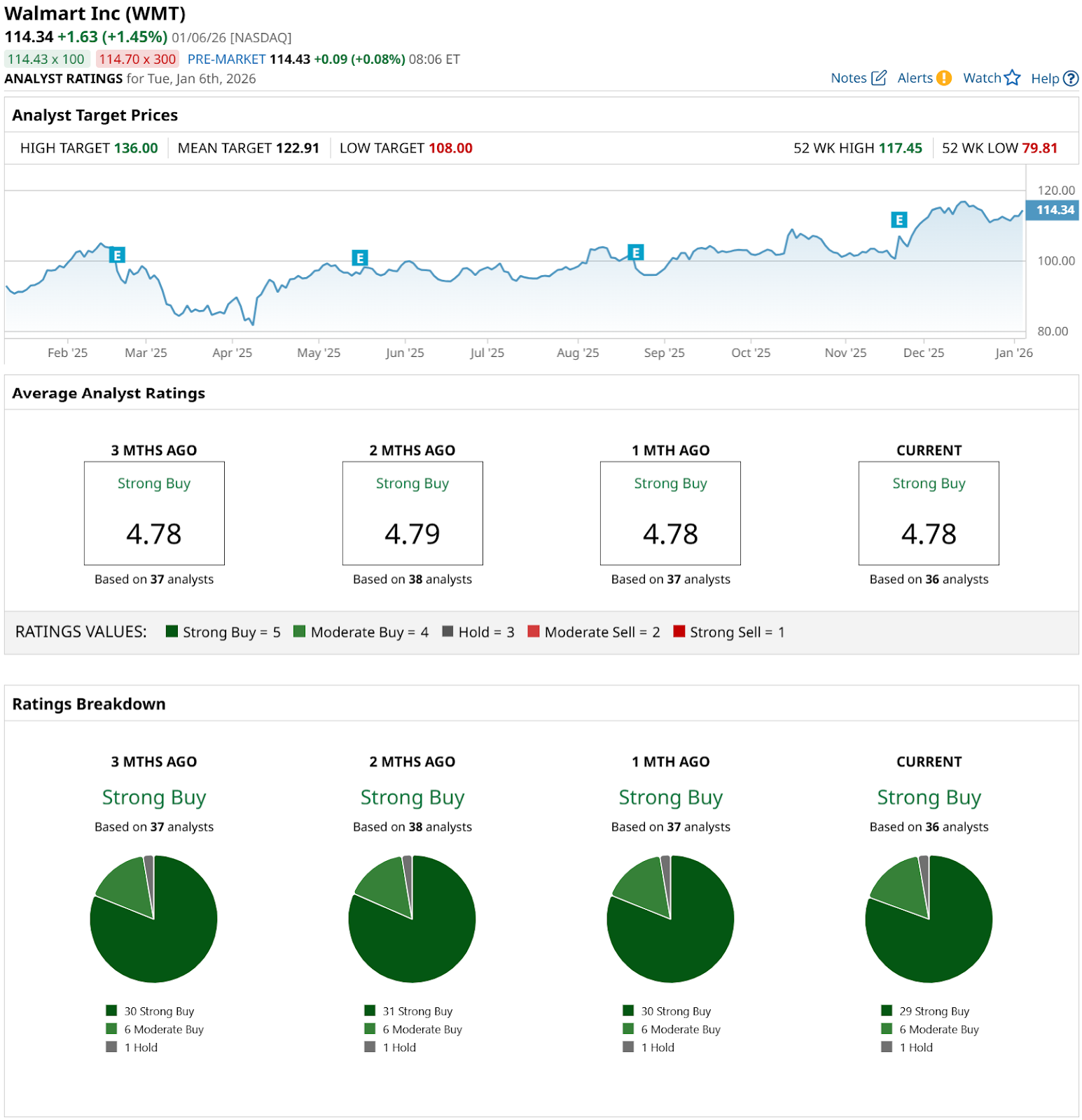

WMT stock is up 23% over the past 52 weeks and up 1.5% year-to-date (YTD), showing investors have continued to favor Walmart’s steady earnings and reliable cash flow in an uncertain market.

However, valuation is no longer cheap. WMT stock’s forward price-to-earnings (P/E) multiple is about 43 times, well above the sector average. Still, the Dividend Aristocrat story is intact here. Walmart has raised its dividend for 52-straight years, and pays quarterly. The company most recently declared a dividend of $0.235 per share, although its yield of 0.82% is below the Consumer Staples average of about 2%.

In fiscal third quarter of 2026, Walmart delivered revenue of $179.5 billion, up 5.8% year-over-year (YOY), and adjusted EPS of $0.58, beating expectations. Management also raised its full-year outlook, calling for net sales growth of 4.8% to 5.1% and adjusted EPS of $2.58 to $2.63.

On the business side, Walmart is also leaning into AI-enabled shopping. It announced a partnership with OpenAI that will let customers shop Walmart through ChatGPT using “Instant Checkout,” which could help it turn more online browsing into purchases. Outside of the United States, Walmart Canada is also expanding its last-mile reach through a delivery partnership that covers more than 300 stores nationwide, helping it stay competitive as delivery becomes more important.

Wall Street remains strongly positive on WMT stock. The 36 analysts with coverage of shares rate WMT a consensus “Strong Buy." The average price target of $123.40 suggests about 9% potential upside from the current price.

The Coca-Cola Company (KO)

The Coca-Cola Company (KO) is a global beverage leader that makes most of its profit by selling concentrates and syrups to a huge bottling network. That setup keeps the business relatively asset-light, while Coca-Cola’s marketing reach helps its brands stay relevant around the world.

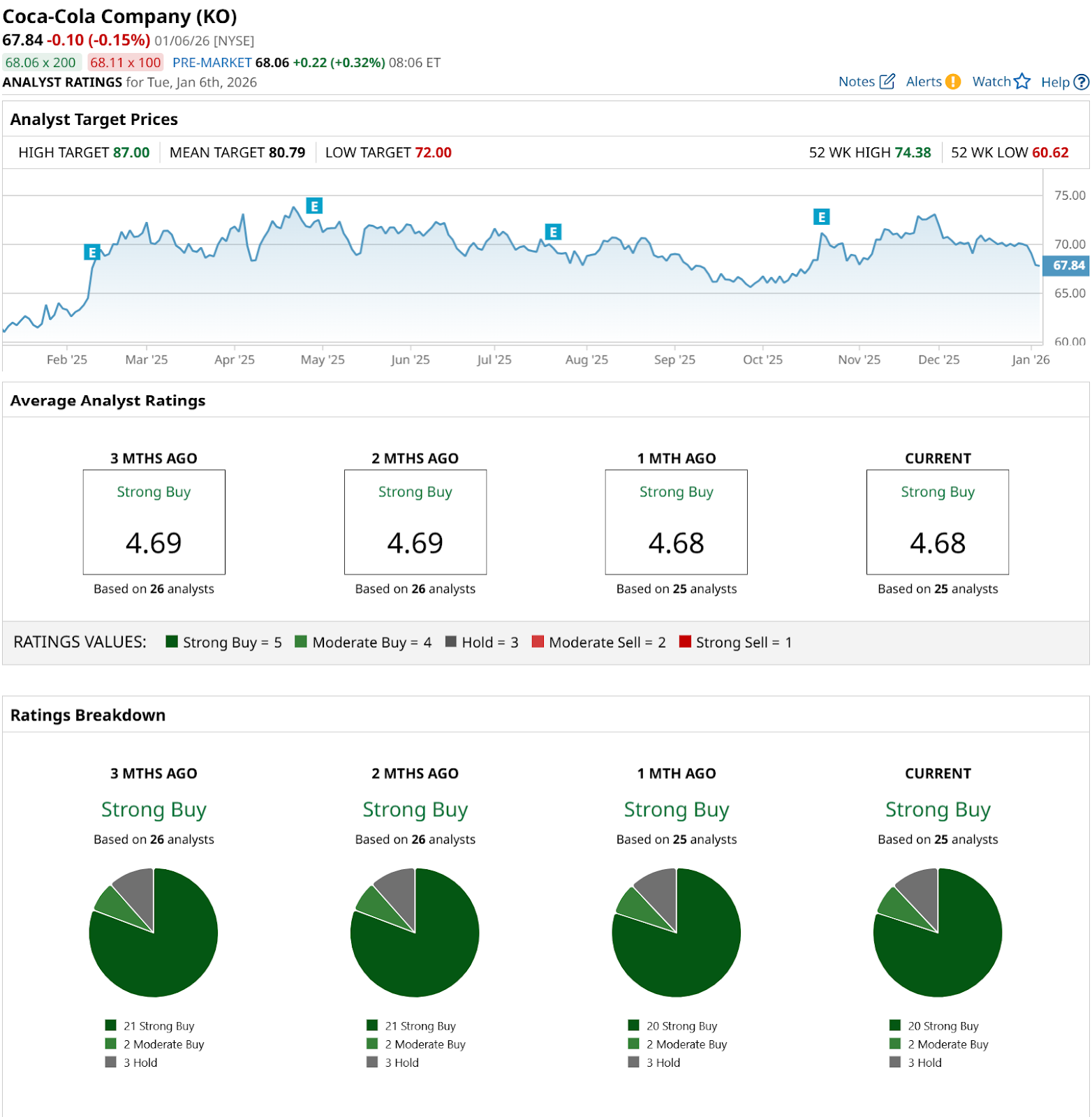

The performance of KO stock lines up with what many dividend investors look for heading into 2026. KO stock is up 12% over the past 52 weeks, although shares are down 1% on a YTD basis.

Valuation is not so stretched, although KO still trades at a premium. The stock's forward P/E is around 21 times, well above the sector average near 15 times.

That said, the Dividend Aristocrat story here also stands out. Coca-Cola has increased its dividend for 63-straight years, recently paying $0.51 per share on Dec. 15. KO offers a yield of 3.01%, above the Consumer Staples average, although the forward payout ratio at 67.64% shows this is a mature company focused on returning cash rather than reinvesting aggressively for growth.

In Q3 2025, net revenues rose 5% to $12.5 billion, organic revenue grew 6%, and adjusted EPS increased 5% to $0.82. On the brand side, Coca-Cola signed a three-year partnership with Manchester United (MANU) as the club’s official carbonated soft drinks partner in the U.K. and Europe, keeping its marketing tied to one of the world’s biggest sports platforms. Distribution is also being strengthened through an exclusive supply deal involving Coca-Cola Canada Bottling, which should help keep Coca-Cola products anchored across foodservice channels.

Analysts remain upbeat, rating KO stock as a consensus “Strong Buy." The $80.83 average price target implies about 16% potential upside from the current price.

Nucor (NUE)

Nucor is North America’s largest steelmaker, and it runs a flexible, scrap-based mini-mill network alongside downstream fabrication. This setup is designed to keep costs competitive and let the company adjust quickly as demand shifts across construction, manufacturing, and energy.

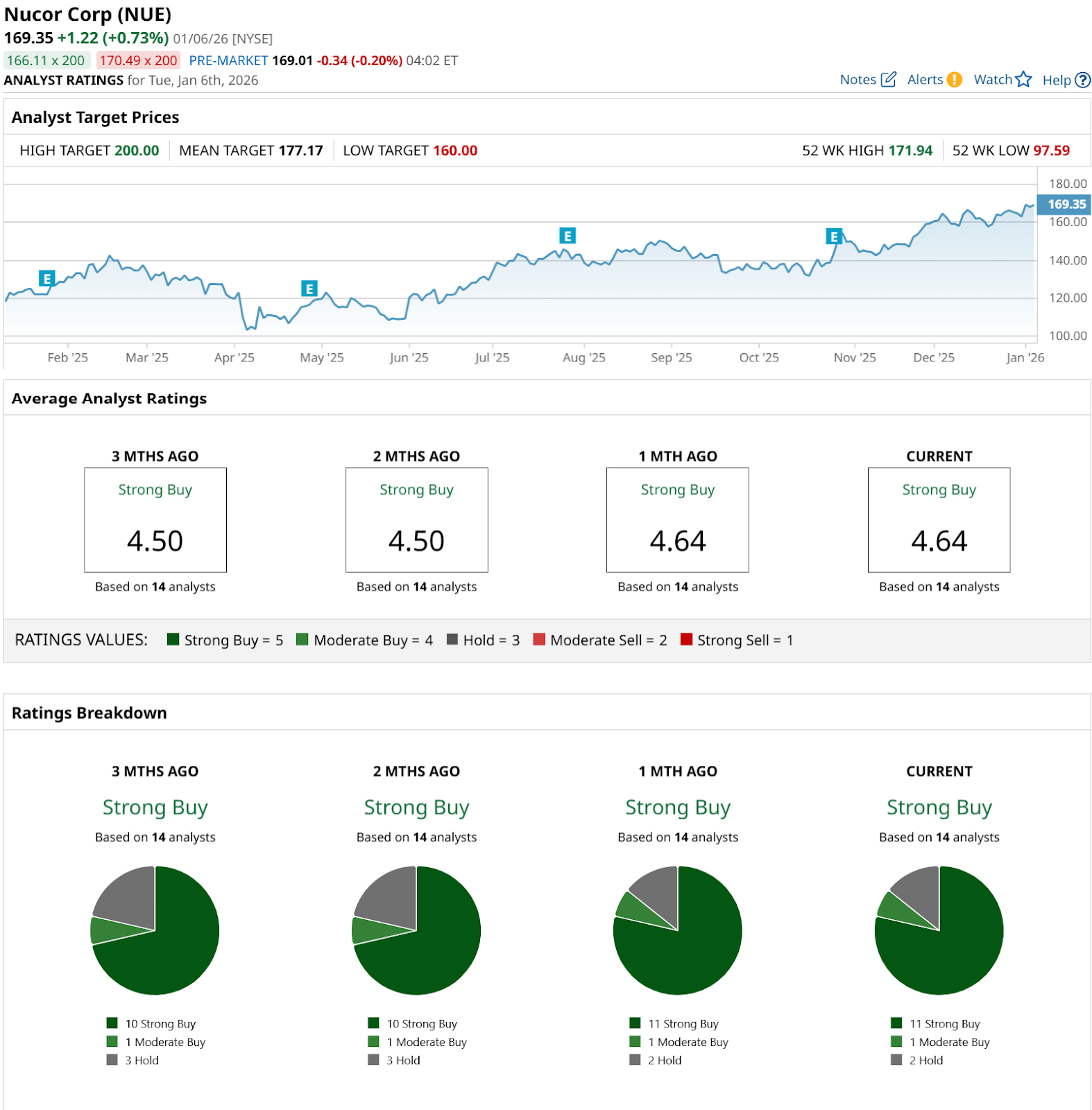

NUE stock is up 42% over the past 52 weeks and up 3% YTD, which shows investors have been leaning toward the idea of a stronger industrial cycle.

The valuation also looks fairly reasonable for a stock with that kind of momentum. Nucor’s forward P/E is about 14.5 times, which is below the broader sector. For dividend investors, NUE also still fits the Dividend Aristocrat profile, with 53-straight years of dividend increases, a recent quarterly dividend of $0.56 to be paid on Feb. 11, and a forward payout ratio around 30.32% that leaves room for flexibility even in a cyclical industry. The tradeoff is yield, since its 1.32% yield sits below the industry average.

Results have remained solid. In Q3 2025, Nucor posted net sales of $8.52 billion and net earnings attributable to stockholders of $607 million, or $2.63 per diluted share. EBITDA came in at $1.27 billion, roughly steady versus Q2 2025 and sharply higher than Q3 2024. On the business front, a collaboration with The Nuclear Company to evaluate NQA-1-certified steel for nuclear-grade work ties NUE stock to long-term nuclear buildout and U.S. supply-chain rebuilding. A separate real estate deal involving a 46,000-square-foot Dallas, Texas property leased to Nucor Rebar also highlights the ongoing demand for its downstream footprint.

Analyst sentiment is positive, with NUE stock having a consensus “Strong Buy" rating. The $178.83 average price target implies about 7% potential upside from the current price.

Conclusion

Walmart, Coca-Cola, and Nucor look like three very different ways to play the same 2026 Dividend Aristocrat thesis: dependable businesses with long dividend-growth streaks, plus broadly bullish analyst sentiment that suggests the market still sees room to run.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- The 3 Best Dividend Aristocrats to Buy for 2026

- As the US Dollar Index Tests Critical Support, Here’s What a Dollar Breakdown Could Mean for Markets

- Trump Wants Lockheed Martin to Cut Its Dividend. Should You Still Buy LMT Stock or Stay Far Away?

- Palantir Is Pulling Back After a Post-Venezuela Run Higher. How Should You Play PLTR Stock Here?