Shareholders of Clean Harbors would probably like to forget the past six months even happened. The stock dropped 21.8% and now trades at $191.03. This might have investors contemplating their next move.

Is now the time to buy Clean Harbors, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Even with the cheaper entry price, we're sitting this one out for now. Here are three reasons why we avoid CLH and a stock we'd rather own.

Why Is Clean Harbors Not Exciting?

Established in 1980, Clean Harbors (NYSE:CLH) provides environmental and industrial services like hazardous and non-hazardous waste disposal and emergency spill cleanups.

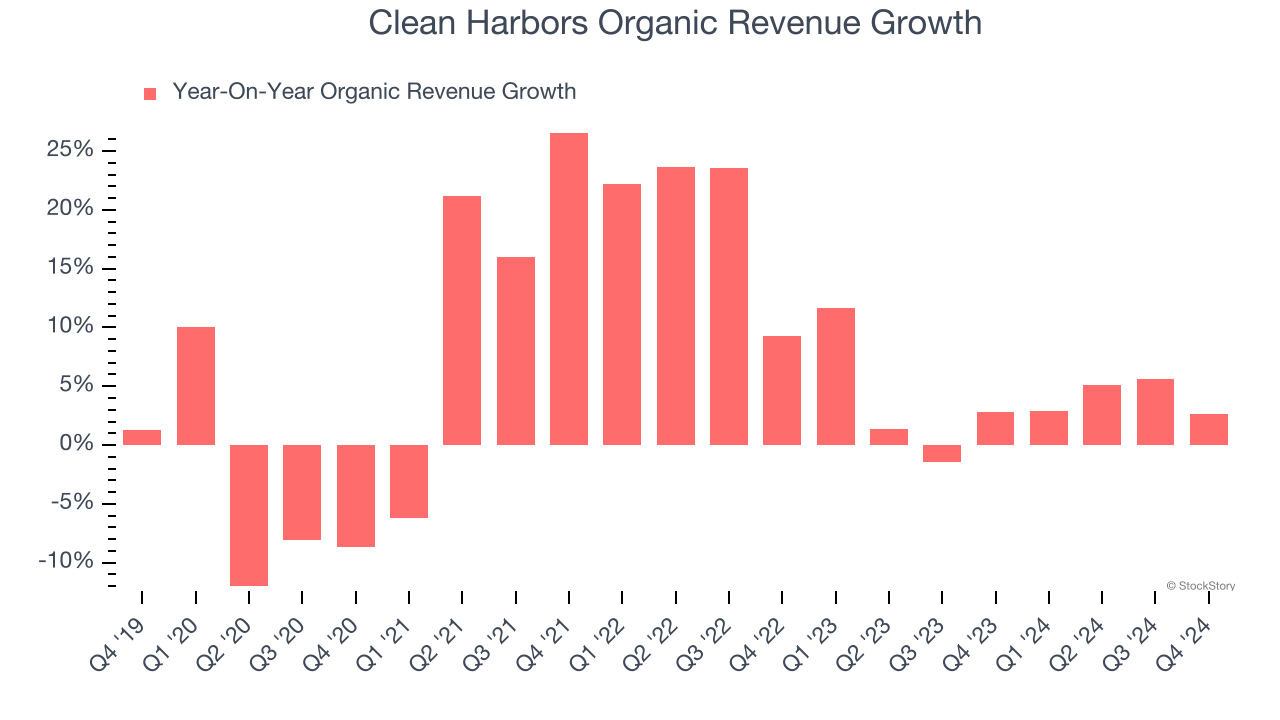

1. Slow Organic Growth Suggests Waning Demand In Core Business

In addition to reported revenue, organic revenue is a useful data point for analyzing Waste Management companies. This metric gives visibility into Clean Harbors’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Clean Harbors’s organic revenue averaged 3.8% year-on-year growth. This performance was underwhelming and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

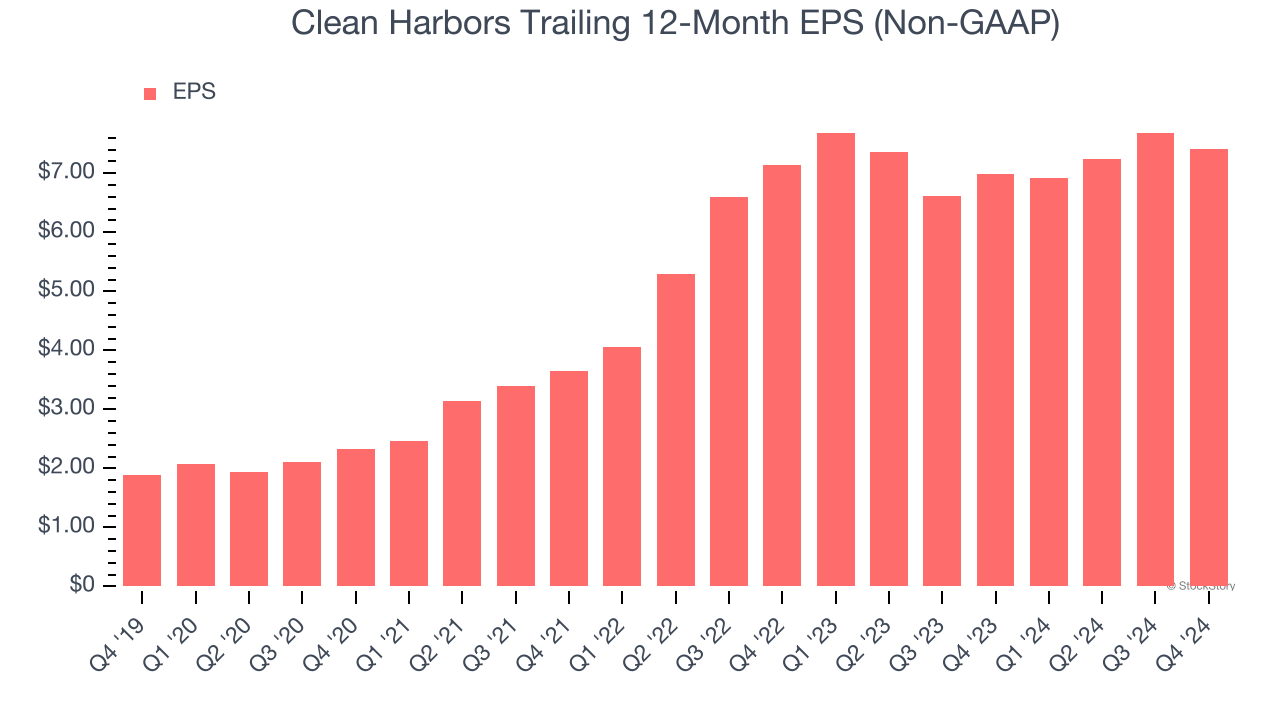

2. Recent EPS Growth Below Our Standards

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Clean Harbors’s EPS grew at a weak 1.9% compounded annual growth rate over the last two years, lower than its 6.8% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

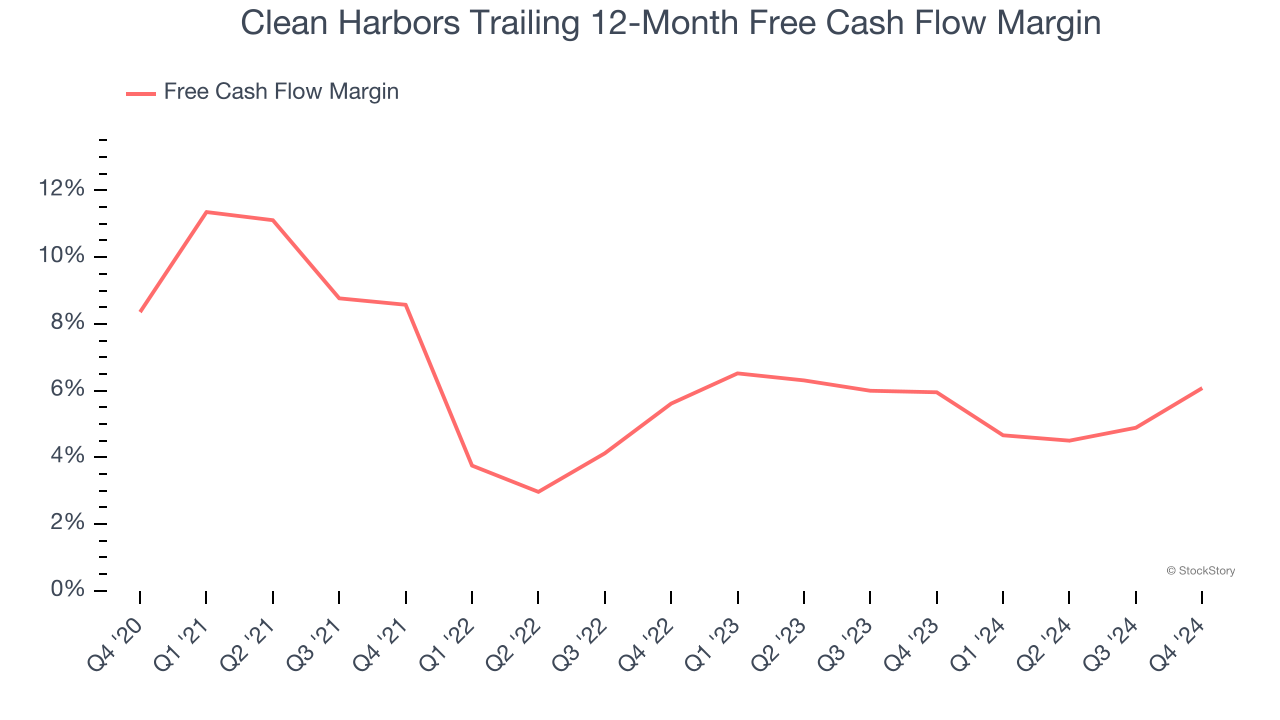

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Clean Harbors’s margin dropped by 2.3 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. Clean Harbors’s free cash flow margin for the trailing 12 months was 6.1%.

Final Judgment

Clean Harbors isn’t a terrible business, but it doesn’t pass our bar. After the recent drawdown, the stock trades at 23× forward price-to-earnings (or $191.03 per share). Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere. Let us point you toward a top digital advertising platform riding the creator economy.

Stocks We Would Buy Instead of Clean Harbors

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.