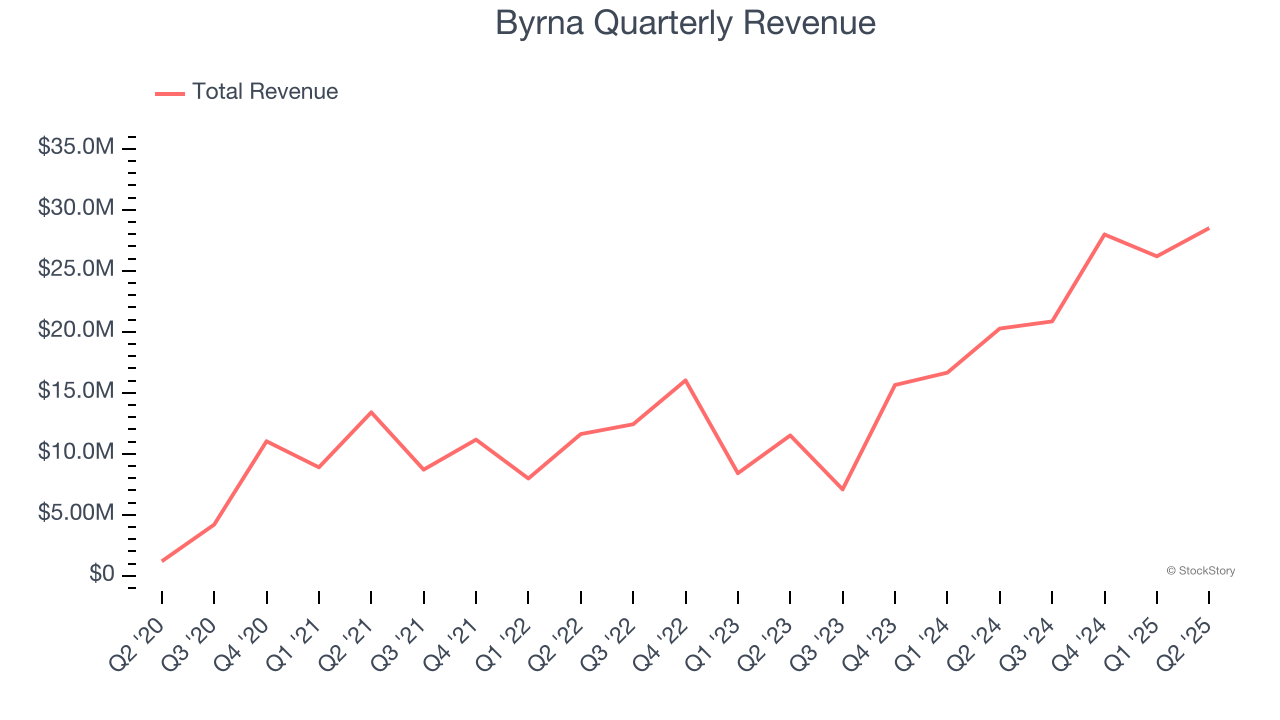

Non-lethal weapons company Byrna (NASDAQ:BYRN) met Wall Street’s revenue expectations in Q2 CY2025, with sales up 40.6% year on year to $28.51 million. Its GAAP profit of $0.10 per share was 42.9% above analysts’ consensus estimates.

Is now the time to buy Byrna? Find out by accessing our full research report, it’s free.

Byrna (BYRN) Q2 CY2025 Highlights:

- Revenue: $28.51 million vs analyst estimates of $28.47 million (40.6% year-on-year growth, in line)

- EPS (GAAP): $0.10 vs analyst estimates of $0.07 (42.9% beat)

- Adjusted EBITDA: $4.3 million vs analyst estimates of $3.17 million (15.1% margin, 35.5% beat)

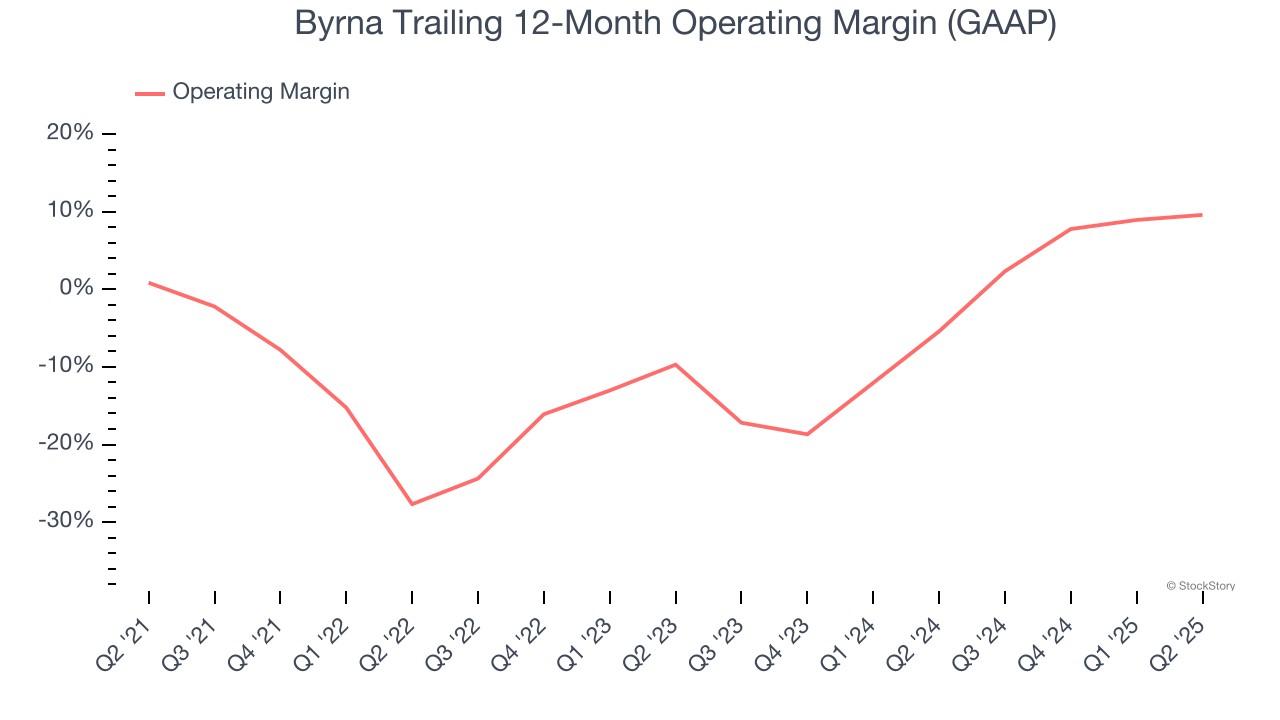

- Operating Margin: 11.7%, up from 9.4% in the same quarter last year

- Market Capitalization: $732.5 million

Byrna CEO Bryan Ganz stated: “The launch of the Byrna CL in May helped us deliver a record $28.5 million in revenue for the second quarter. Despite overall softness in consumer spending, our focused marketing and retail expansion strategies allowed us to continue growing our total addressable market and reach new milestones. Looking ahead, we expect that the CL will be a larger part of our sales mix, especially now that it is available to customers on Amazon."

Company Overview

Providing civilians with tools to disable, disarm, and deter would-be assailants, Byrna (NASDAQ:BYRN) is a provider of non-lethal weapons.

Revenue Growth

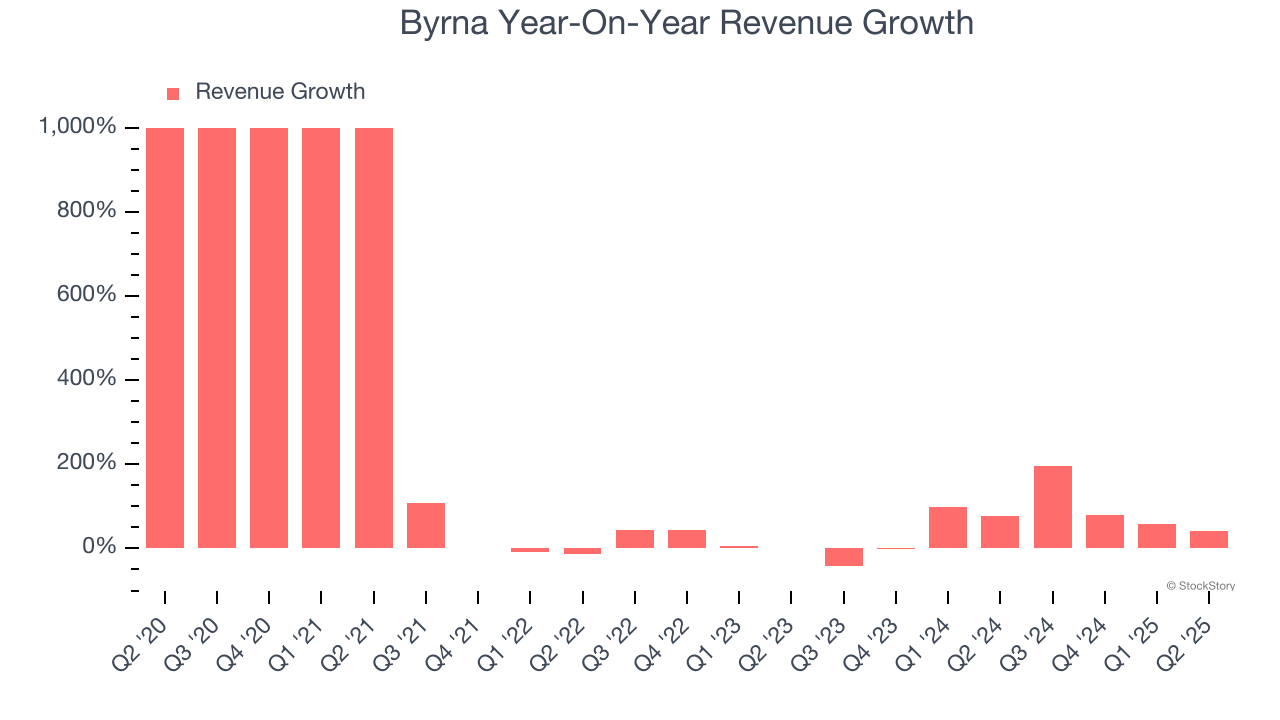

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, Byrna’s sales grew at an incredible 28.9% compounded annual growth rate over the last five years. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Byrna’s annualized revenue growth of 46.3% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated. We note Byrna isn’t alone in its success as the Law Enforcement Suppliers industry experienced a boom, with many similar businesses also posting double-digit growth.

This quarter, Byrna’s year-on-year revenue growth of 40.6% was magnificent, and its $28.51 million of revenue was in line with Wall Street’s estimates.

We also like to judge companies based on their projected revenue growth, but not enough Wall Street analysts cover the company for it to have reliable consensus estimates. This signals Byrna could be a hidden gem because it doesn’t get attention from professional brokers.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

Although Byrna was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 3% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out.

On the plus side, Byrna’s operating margin rose by 8.8 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to show consistent profitability.

This quarter, Byrna generated an operating margin profit margin of 11.7%, up 2.2 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

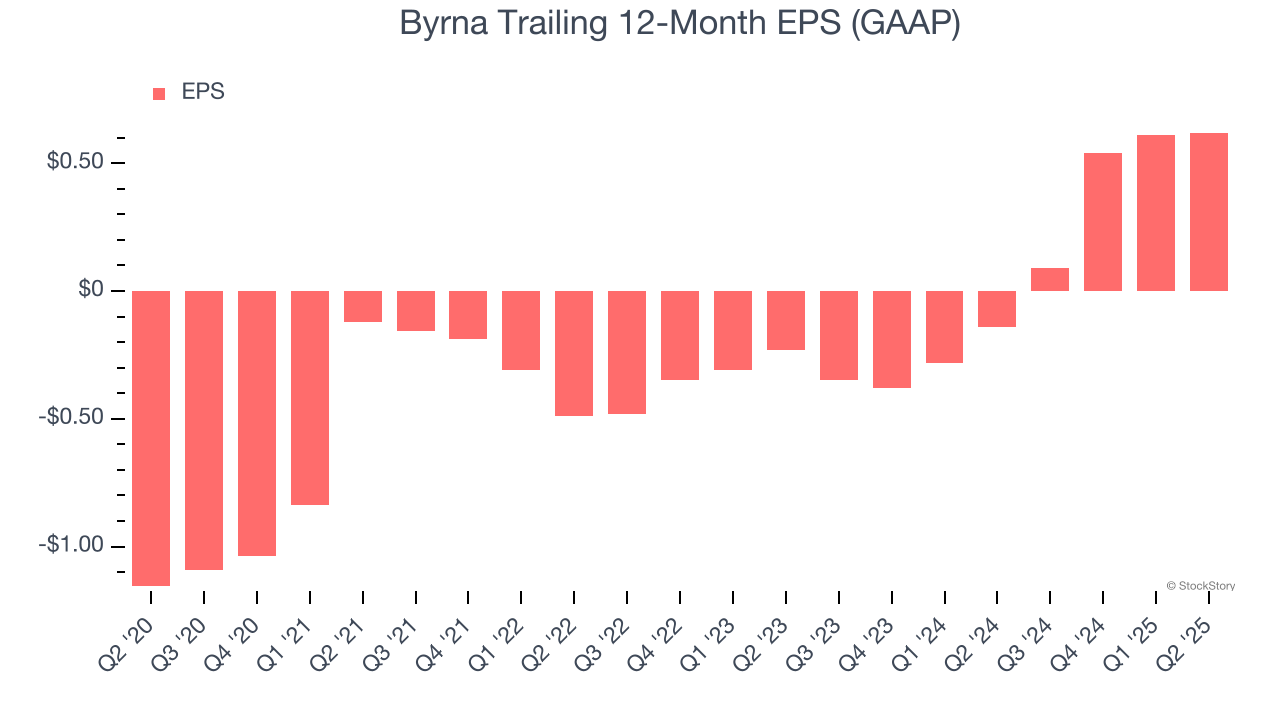

Byrna’s full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it’s at an inflection point.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Byrna, its two-year annual EPS growth of 117% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q2, Byrna reported EPS at $0.10, up from $0.09 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data. This signals Byrna could be a hidden gem because it doesn’t have much coverage among professional brokers.

Key Takeaways from Byrna’s Q2 Results

We were impressed by how significantly Byrna blew past analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock remained flat at $32.48 immediately after reporting.

Sure, Byrna had a solid quarter, but if we look at the bigger picture, is this stock a buy? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.